The Wealthy Pauper:Why Indian Retirees Struggle to Spend What They Saved

Mr. Sharma (a pseudonym for perhaps your father, uncle, or neighbor) is a success story of the great Indian middle-class dream.

He grew up in an India of scarcity—ration cards, waiting years for a telephone connection, and job security being the ultimate prize. For 40 years, he worked tirelessly in a PSU or a corporate job. He walked to the bus stop to save the autorickshaw fare. He wore shirts until the collars frayed. He sacrificed vacations to pay for IIT coaching and his children’s grand weddings.

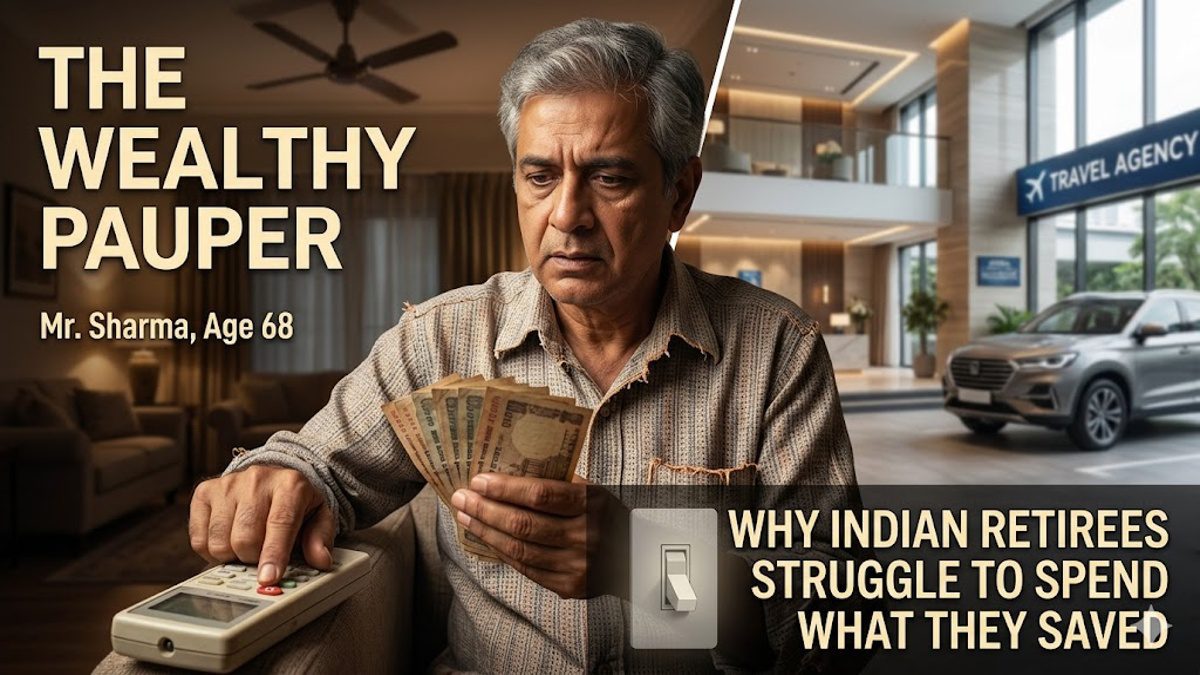

Today, at 68, Mr. Sharma is sitting on a paid-off house in a decent locality and a retirement corpus of over ₹1.5 Crores in FDs, PPF, and mutual funds. He has won the game. He is financially free.

Yet, last night in the peak of the May summer heat, Mr. Sharma woke up sweating because he switched off the AC after running it for exactly one hour. “Why waste electricity?” he murmured.

This is the tragedy of the modern Indian retiree. They are asset-rich and cash-rich, but lifestyle-poor. They are suffering from what financial psychologists call The Switch Failure—the psychological inability to transition from saving to spending.

The Psychology of the Eternal Saver

For four decades, the switch in their brain was welded tight to the SAVE position. Every financial decision was filtered through the lens of accumulation. Saving wasn’t just a habit; it was a survival mechanism against an uncertain future in a developing economy.

Then, on the day of retirement, they are suddenly told to flip that switch to SPEND. They physically cannot do it. The neural pathways built over 40 years of frugality are too strong. To a lifelong saver, spending money—specifically, “decumulating” their hard-earned principal—registers in the brain almost like physical pain or moral failure. They feel they are chopping down the tree they spent their whole life watering.

Symptoms of The Switch Failure in India

You see this manifested in countless Indian households where parents have more than enough money, yet live in self-imposed austerity:

-

The FD Interest Trap: They will only spend the interest earned from Fixed Deposits. Touching the principal amount feels like committing a sin. As inflation rises, their lifestyle shrinks even though the principal remains untouched.

-

The Medical Delay: They will have crores in the bank but will delay a necessary knee replacement or cataract operation for years because it “costs too much right now.”

-

The Travel Paradox: At 70 years old, with bad backs, they still book Sleeper Class train tickets for overnight journeys instead of a comfortable 2AC or a flight, simply because “the train gets us there too.”

-

The Inheritance Burden: A uniquely Indian pressure is the deep-seated belief that the entire corpus must be preserved for the children. They live like paupers so their 45-year-old, well-settled children can inherit a massive fortune later.

The Great Fear: What if I live too long?

The engine driving this inability to spend is a deep, primal fear of running out of money. Indian retirees have seen inflation destroy the value of the Rupee over decades. They don’t trust that ₹1.5 Crores today will be enough 20 years from now when a hospital room might cost ₹50,000 a night.

So, they create a hyper-conservative buffer. They prepare for the absolute worst-case scenario (living to 105 with major medical needs), and in doing so, they completely miss out on the best-case scenario—enjoying the healthy years they have left.

The Final Destination: The Richest Corpse

The tragic outcome of The Switch Failure is a life unlived. They sacrificed their 30s, 40s, and 50s for a “someday” of comfort. But when the day arrives, they are too psychologically conditioned by scarcity to embrace it.

They become the richest people in the graveyard. They leave behind massive bank balances, perfectly preserved houses, and unspent lockers full of gold jewelry. Their children inherit wealth they often don’t urgently need, while the parents die with regrets of trips not taken and comforts not bought.

Flipping the Switch: How to Enjoy the Harvest

If you, or your parents, are stuck in this trap, logic won’t fix it. Emotional re-framing is needed:

-

The Permission to Spend Fund: Create a separate bank account funded by a small portion of the corpus. The rule is simple: This money must be “wasted.” It cannot be saved or given to kids. It must be spent on frivolous joy—a luxury hotel, a new car, or a hobby.

-

The Bucket Strategy: Divide the wealth. Bucket A is untouchable survival money for medical needs and basic living until age 90. Bucket B is lifestyle money. Once Bucket A is secure, the brain relaxes, making it easier to spend from Bucket B without panic.

-

Shift the Inheritance Perspective: The greatest gift a parent can give adult children isn’t a massive inheritance when the children are already 50. The greatest gift is being happy, healthy, and financially independent parents who enjoy their own lives.

The Bottom Line:

Money is stored energy. You spent your life accumulating this energy. If you don’t release it in the form of joy, comfort, and experiences while you are alive, that energy goes to waste.

You didn’t work for 40 years just to be the wealthiest patient in the hospital ward. Don’t remain The Wealthy Pauper: Why Indian Retirees Struggle to Spend What They Saved. Flip the switch. Buy the ticket. Turn on the AC. You earned it.